ZET Momentum Rebounds: State Leadership Is Shaping Where Adoption Accelerates

By Cristy Almonte

The U.S. zero-emission truck (ZET) market just doubled its pace. In the second half of 2025, fleets deployed nearly twice as many ZETs as in the first 6 months of the year — signaling a fundamental shift in how American fleets think about electrification. CALSTART’s June 2026 Zeroing in on Zero-Emission Trucks (ZIO ZET) Market Update explores what drove that momentum and how deployment patterns are shifting across vehicle segments, states, and use cases.

By the end of 2025, cumulative ZET deployments in the United States reached 72,309 vehicles. The market saw a strong rebound from July through December, adding 12,996 deployments during that 6-month period, nearly double the 6,526 deployments added in the first half of 2025. ZETs also represented 4.14% of all truck deployments during the second half of 2025, the strongest 6-month deployment share recorded to date.

These figures point to a market that is not only growing but becoming more resilient. The full ZIO ZET Market Update explores where the momentum is coming from, which segments are leading, and why adoption is accelerating faster in some states than others.

Cargo Vans Continue To Anchor Growth

Zero-emission cargo vans.

Cargo vans continued to drive much of the market’s growth. Their predictable routes, lower infrastructure complexity, and clear operational fit make them one of the most accessible entry points for fleet electrification. After a slower first half of the year, the segment rebounded sharply in the second half, helping drive the strongest 6-month ZET deployment share recorded to date.

Cargo vans are not just leading the market by volume — they’re showing what early ZET momentum looks like when a segment is ready to scale. Their growth shows adoption can move quickly when fleets have a clear use case, confidence in the technology, and a practical path to deployment.

Refuse Trucks Ready for Takeoff?

Growth is also occurring in other segments, with refuse trucks, yard tractors, and medium-duty step vans continuing to make progress. Refuse trucks saw a noticeable increase in deployment share from the previous report, reaching 3.02%. This momentum suggests that refuse trucks may be emerging as one of the next leading vocational segments.

Refuse trucks represent a more demanding vocational use case, but one that may be well suited for electrification. Their stop-and-go routes and predictable operating patterns create opportunities for regenerative braking, while early deployments have pointed to benefits such as lower vehicle downtime and strong performance in daily operations.

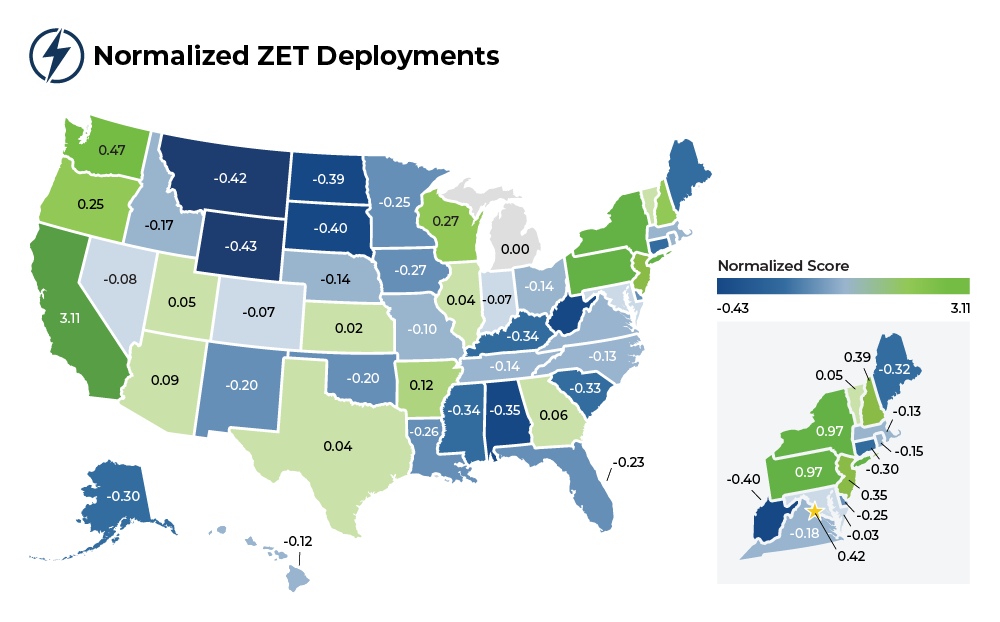

More States Are Deploying ZETs, But Progress Remains Uneven

Twenty-two states now have more than 1,000 cumulative ZET deployments, up from 18 in the previous market update. That milestone suggests the market is no longer limited to a few early leaders.

Still, raw deployment totals can be misleading. California, Florida, and Texas were the top three states for cumulative ZET deployments, reflecting their large truck populations and major freight activity. However, large truck markets can make some states appear farther ahead than their relative progress suggests. To better understand adoption relative to market size, CALSTART’s latest update also examines normalized ZET deployment scores.

This normalized view is especially useful for policymakers and industry stakeholders. By adjusting truck stock, vehicle segment, and fleet size, the analysis provides a more balanced view of which states are performing above the national average and which markets may need additional support.

In this update, California, New York, and Pennsylvania lead the country in normalized ZET deployment scores. California’s leadership reflects a mature policy and market ecosystem, including vehicle incentives, infrastructure support, and market-development policies. New York and Pennsylvania are notable because their performance reflects more than total vehicle counts. Both states are showing progress across a more diverse mix of vehicle segments and have taken steps to support adoption through incentives, workforce development, infrastructure planning, and statewide clean transportation efforts.

How states rank on CALSTART’s normalized ZET score according to the June 2026 report.

Success Defined by State Leadership

The normalized results reinforce a key lesson: The next phase of ZET adoption won’t only be defined by how many vehicles are deployed, but whether states are creating the conditions for fleets to adopt ZETs across a wider range of use cases. Supportive policy, reliable funding, infrastructure readiness, fleet education, and market confidence will influence whether deployments expand beyond easier-to-electrify segments into the broader commercial truck market.

The contrast between cumulative and normalized performance also shows that state leadership matters. Florida and Texas remain among the leading states by cumulative deployment totals, but their normalized performance tells a more nuanced story. Much of their activity is concentrated in cargo vans, and adoption is not keeping pace with the size of their overall truck markets.

For stakeholders working to accelerate zero-emission freight, the June 2026 ZIO ZET report offers a clearer view of where the market stands and where it may be headed. The data points to continued momentum, though growth is not evenly distributed. States that combine policy and financial support, infrastructure planning, and fleet education are better positioned to turn early deployment activity into broader market growth.

Read the full June 2026 ZIO ZET Market Update here and explore the complete deployment data, normalized state-level analysis, segment trends, and factors shaping where ZET adoption is accelerating across the country.

Cristy Almonte is a technical project manager on the Trucks team at CALSTART.