Zeroing in on Zero-Emission Trucks

Zeroing in on Zero-Emission Trucks highlights the continued increase in medium- and heavy-duty (MHD) zero-emission truck (ZET) deployments in the United States. This series provides a concise and current snapshot of ZET deployment statistics and the existing U.S. MHD truck market. These reports offer insights into key trends driving growth in ZET adoption, as well as opportunities to further accelerate this growth that can help inform policymakers, original equipment manufacturers, fleet owners, and financial stakeholders.

Download the Report

ZET Dashboard

Insights

Download the Report

ZET Dashboard

Insights

Latest Market Update

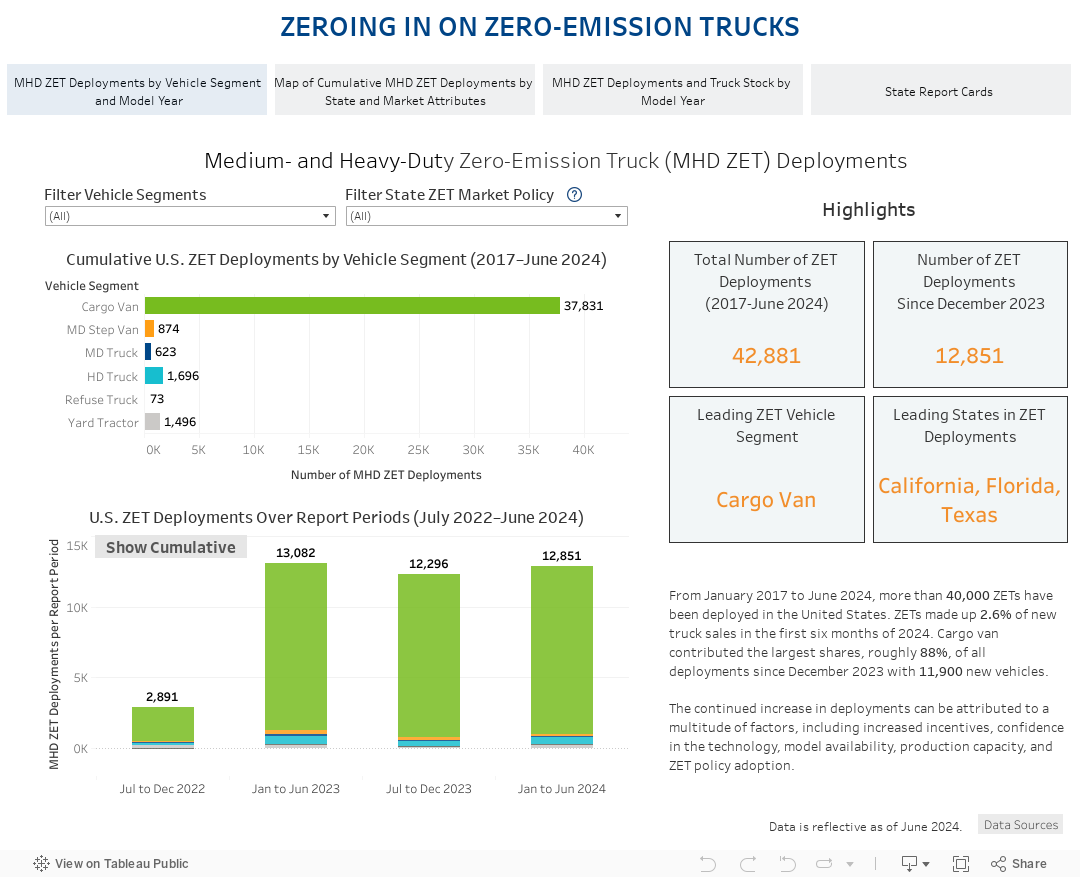

The June 2026 Zeroing in on Zero-Emission Trucks (ZIO ZET) Market Update points to renewed momentum in the U.S. medium- and heavy-duty ZET market. After a slower start to 2025, deployments accelerated in the second half of the year, with ZETs representing 4.14% of all truck deployments from July through December, up from 1.32% in the first half of 2025. This acceleration brought cumulative ZET deployments to 72,309 vehicles nationwide by December 2025. While cargo vans continued to drive much of this growth, the broader story is one of a maturing market: Fleets are gaining confidence, adoption is spreading across more applications, and state leadership continues to shape where the transition is gaining ground fastest.

Beyond cargo vans, the latest data shows continued progress across several medium- and heavy-duty applications. Yard tractors remain the leading segment for zero-emission market share, while refuse trucks and medium-duty step vans showed increased deployment shares compared with the previous report. Most importantly, the data reinforces that state leadership continues to shape the market. California, New York, and Pennsylvania lead in normalized adoption, which demonstrates that supporting the ZET ecosystem through supportive policy, as outlined in the ZET Ahead Dashboard, can help accelerate ZET deployment relative to market size. Looking ahead, continued progress will depend on aligning policy, infrastructure investment, financing solutions, and fleet engagement to make ZET deployments more practical nationwide.

Key Insights

The second half of 2025 marked the strongest 6-month deployment period for ZETs to date. There were 12,996 new ZET deployments from July through December, nearly double the 6,526 deployments added in the first half of the year. This rebound shows that, despite a slower start to 2025, deployment momentum continued to build, driven in part by greater business certainty and growing confidence in zero-emission technology. Cargo vans continued to drive the majority of market growth, with 12,158 new deployments in the second half of 2025. Their rebound reflects the segment’s relative maturity, lower deployment barriers, and strong fit for many fleet duty cycles. At the same time, ZET adoption is becoming less narrowly concentrated than in earlier years, with yard tractors, refuse trucks, and medium-duty step vans showing continued progress.

State-level results show two different but important stories. California, Florida, and Texas continue to lead in total cumulative deployments, reflecting their large truck markets. However, when deployment activity is normalized by truck stock, vehicle segment, and fleet-size mix, California, New York, and Pennsylvania emerge as the strongest performers relative to the national average. This shows implementing state policy that supports ZET deployments helps accelerate adoption beyond what a state’s market size alone would predict. Dive into the full report to explore what these leading states are doing differently and how they’re driving ZET adoption.

To sustain deployment momentum, states and industry leaders should prioritize:

- Supporting financing assistance to reduce risk for fleets and make ZET adoption more accessible.

- Accelerating infrastructure deployment through shared hubs, flexible interconnection solutions, greater utility coordination, and work-around solutions such as microgrids and mobile charging.

- Providing long-term policy certainty through coordinated planning, clear market signals, and sustained public–private collaboration.

- Continuing deep outreach and education about the benefits of ZETs with shippers, carriers, dealers, utilities, and other stakeholders and how everyone can work together to continue adoption.

Overall, this update points to a zero-emission market that is still advancing despite a period of slower deployment activity in the first half of the year. Continued growth will depend on whether states, fleets, utilities, infrastructure providers, and manufacturers can work together to reduce deployment barriers and make ZETs a viable business choice across more vehicle segments and geographies.

Past Reports

Browse the links below for the full library of Zeroing in on ZETs reports and market updates.

January 2026

June 2025

January 2025

May 2024

January 2024

May 2023

June 2022

January 2022

Resources

Browse the links below for additional resources like fact sheets, blogs, publications, and more.

ZETs: The Facts

This fact sheet provides a concise overview of the state of zero-emission freight vehicles in the United States, including industry demand, supply, and benefits.

National ZE MHD

Infrastructure Map

Find publicly available chargers and hydrogen refueling stations for your zero-emission class 2b-8 trucks.

ZET Ahead

Dashboard

Provides policymakers, industry, and advocates alike with a snapshot of the actions driving success in states committed to a rapid transition to zero-emission trucks (ZETs) and buses.

Innovative

Financing Toolkit

This toolkit showcases valuable knowledge products developed by CALSTART to catalyze investment in the zero-emission transportation sector.

Phasing in

U.S. Charging

Infrastructure

Phasing in U.S. Charging Infrastructure presents a vision and roadmap for how the United States can build out infrastructure to support rapid zero-emission medium- and heavy-duty vehicle (ZE-MHDV) adoption.

MHD EV

Deployment Data

With support from the Department of Energy (DOE), CALSTART and its partners collect and analyze data from a diverse set of electric vehicles (EVs) across different applications, geographies, terrains, and climatic conditions.

Shared Charging

This FAQ-style report answers the most common questions about shared charging sites.